Crypto Loans vs. Credit Lines: What Matters When Markets Turn Volatile

Borrowing is a strong alternative to selling crypto - you can withdraw cash, keep the upside, and avoid a tax event. But grabbing the first offer that looks decent isn't a wise move.

The difference between a traditional crypto loan and a credit line matters more than most people realize, especially when markets get volatile and you need room to maneuver.

Let's break down how each works and when they make sense.

TL;DR

- Both let you access cash without selling.

- LTV is the key metric for both. Lower ratio = lower rates, less risk.

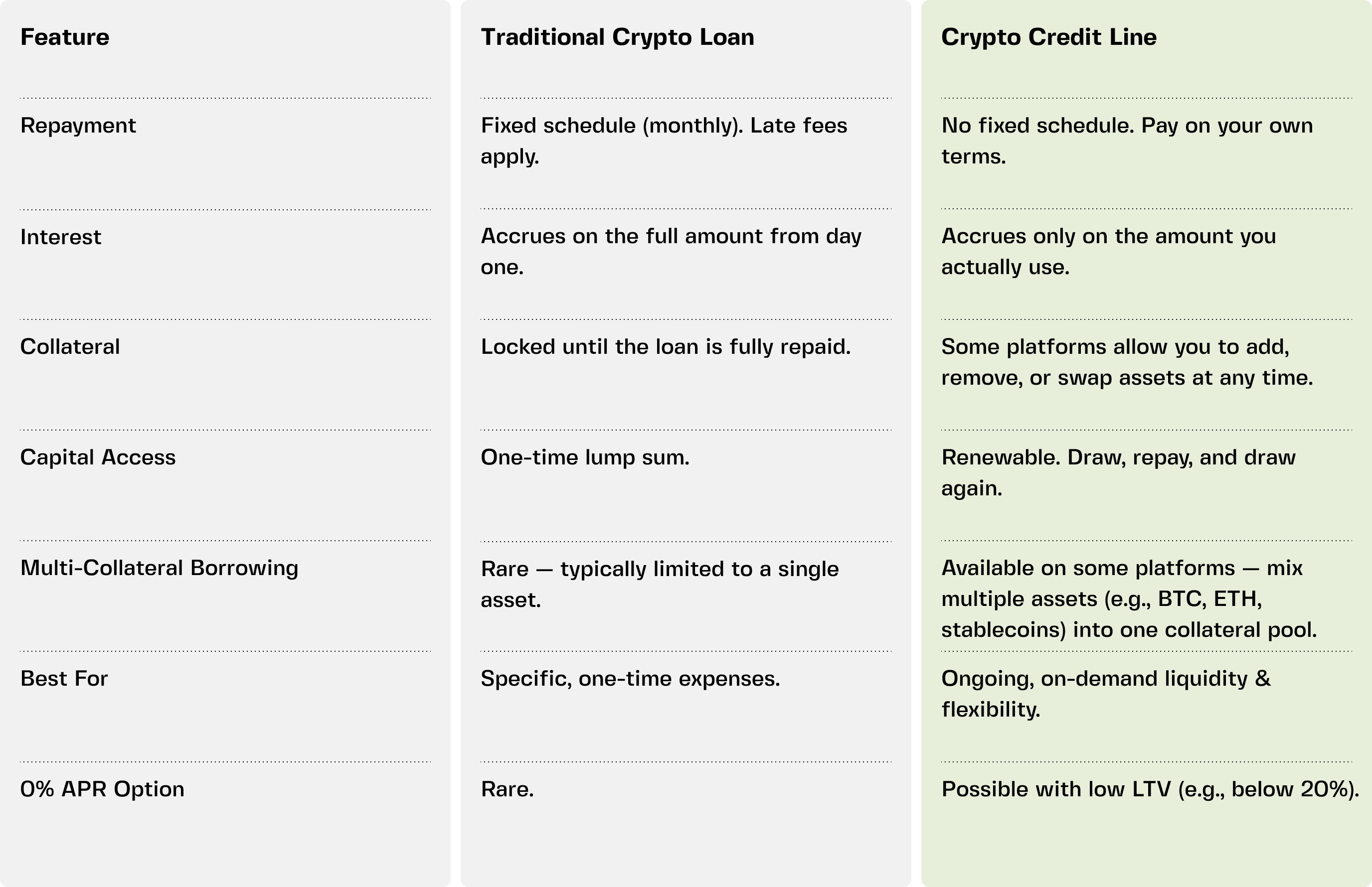

- Traditional loans give you a lump sum with fixed repayments. Your collateral stays locked until you fully repay.

- Credit lines are renewable. Draw what you need, pay interest only on what you use.

- Some credit lines keep your collateral accessible - you can swap assets without closing the line. Traditional loans freeze your collateral until repayment.

- Credit lines are currently a CeFi product. DeFi offers loans, but with no margin call alerts and no customer support.

What They Have in Common

Crypto loans and credit lines share a few fundamentals. Both:

- Let you access cash without selling your crypto. You keep your position, avoid a taxable event, and still get the liquidity you need. Selling triggers capital gains tax in most jurisdictions.

- Use one or more cryptocurrencies as collateral. You deposit BTC, ETH, or stablecoins, and the platform lends against them. Your loan-to-value ratio (LTV) determines how much you can borrow.

- Reward responsible borrowing. Lower LTV means lower interest rates. The safer your position, the less you pay.

Most centralized lenders provide warnings before liquidation. When your LTV climbs too high, you get an alert to add collateral or repay part of the borrowed amount. Ignore it, and you risk losing your position.

Where They Diverge

Repayment: Fixed Schedule vs. Your Own Terms

A traditional crypto loan locks you into a fixed schedule, typically with monthly payments and a set end date (usually 3–36 months). Missing a payment triggers late fees, regardless of market conditions.

A credit line has no fixed repayment schedule. Borrow when you need to and repay when it suits you, as long as your LTV stays in the safe zone. No monthly minimums or penalties for early repayment. Return what you owe and keep the line open for next time.

Access to Your Collateral: Flexible vs. Locked

With a traditional loan, your collateral stays locked until you fully repay. Freeing it faster requires early repayment.

With a credit line, your collateral stays accessible - at least on platforms designed for flexibility. You can add, remove, or swap assets without closing the line. That means you can react to market moves without disrupting your liquidity.

For example, if you pledged ETH but want to rotate into SOL, you can swap those assets if your platform allows it. If you worry about a crash, you can instantly add stablecoins to the collateral pool.

How Much You Can Borrow (and When)

A traditional loan gives you a lump sum once. If you need more later, you open another loan - with another approval process and a new lock-up period.

A credit line is renewable. You draw what you need, repay, and the capital is available again. It's always on hand.

Interest Costs: 0% APR Is Rare

Both charge interest, but with some credit line providers, if you keep LTV low (say, 20% or below), your interest rate drops to 0% APR.

Traditional loans rarely offer zero interest. You pay from day one, even if you don't need the whole lump sum - and even if the money sits idle in your account.

CeFi vs. DeFi: Where Credit Lines Live

Crypto credit lines are currently a CeFi (centralized finance) product. You won't find them in DeFi — at least not with the same features.

DeFi offers loans, not credit lines. And DeFi has no margin call alerts or customer support. The moment your health factor (DeFi’s equivalent of LTV) drops below the threshold, a bot liquidates you instantly.

Multi-collateral options also exist in DeFi - but risk management for such positions requires sophisticated tools. CeFi platforms provide warnings, time to act, and customer support. That convenience, however, means borrowers should choose reputable, licensed providers with transparent risk management practices.

When to Use Each

Choose a traditional crypto loan when you:

- Need a specific amount for a one-time expense (car repair, business investment, tax payment)

- Prefer fixed monthly payments and a clear payoff date

- Are comfortable locking your collateral until the loan ends

- Don't need flexibility - just predictability

Choose a crypto credit line when you:

- Want ongoing, on-demand liquidity

- Aren’t sure exactly how much you'll need or when

- Want to pay interest only on what you actually use

- Value the ability to swap collateral without closing the line

- Need access to capital that resets as you repay

- Want a safety net that costs nothing if you keep LTV low

Many people use both. Keep a credit line for emergencies and ongoing needs, and take a fixed loan when you have a specific, one-off expense.

The Multi-Collateral Difference

Most traditional loans limit you to a single asset. You pledge BTC and borrow against BTC.

Some credit lines let you deposit multiple tokens into a single collateral pool - for example, up to 25 assets on Clapp. BTC, ETH, stablecoins, even fiat, all mixed together. This brings several advantages:

- Better borrowing power. Stablecoins have higher LTV limits than volatile assets. Mix them together, and your overall capacity improves.

- Less liquidation risk. If one asset drops, others in your pool can buffer your LTV.

- Flexibility. You can adjust your collateral mix as your market outlook changes - without closing your line.

Bottom Line

Traditional crypto loans are simple and predictable. They work well for one-off needs where you know exactly how much you need and when you can repay.

But if you want flexibility - on-demand access, interest only on what you use, and the ability to adapt as markets move - a credit line is a different tool entirely.

Whichever you choose, borrow conservatively and keep your LTV low, because life (and markets) don’t follow a straight path.

Traditional Crypto Loan vs. Crypto Credit Line